dYdX: Perpetual Futures Exchange

2022-09-02 • Kaleb Rasmussen

GM everyone! Today, we’re going to look at dYdX, a decentralized exchange that combines centralized off-chain order books with decentralized on-chain settlement. All in a noncustodial manner, dYdX enables leveraged perpetual contract trading for over 35 crypto assets. We’ll be exploring perpetual futures, how perpetuals work on dYdX, and specifically, recent dYdX governance updates.

It is important to note that trading perpetuals on dYdX is not allowed for US residents and Blockchain @ GT does not endorse or advocate any illegal conduct.

Intro to Perpetual Contracts and Leverage

Before we dive right into dYdX, let’s answer the question, “What exactly is a perpetual contract?” Well, first, let’s explain what a futures contract is. A futures contract is an agreement to buy or sell an asset at a specific price on a specific date (the expiration date) in the future.

Perpetuals are just futures contracts that have no expiration date. These contracts are also typically bought on margin. What this means is that users leverage themselves by borrowing contracts. In addition, users must lock up a certain amount of collateral (known as initial margin) as a deposit to cover losses in order to open a position (buy or sell a contract).

You may be wondering, why would someone want access to leverage? Or what utility does this bring to users? Leverage allows users the ability to magnify their gains or losses on a given position. If an individual has a high conviction on a particular trade, they can gain more exposure through these mechanics. For example, if you invest $10 in 1 contract, and the contract goes up $1, you’ve made $1. But if you use $10 at 10x leverage, you can buy 10 contracts worth $100. If 1 contract goes up $1, you make $10 (doubled your investment). However, leverage is a double-edged sword. If 1 contract decreased by $1, you would’ve lost all $10 or your entire investment.

How dYdX Works

By collaborating with Starkware, dYdX v3 is able to offer a layer 2 system using zero-knowledge proofs to settle their perpetual contract trades. If you’re unfamiliar with zero-knowledge proofs, reference this great article here. This offers traders much higher trade throughput and lower minimum order sizes, as opposed to just settling trades directly on Ethereum. However, moving forward dYdX will develop its v4 as its own blockchain as a part of the Cosmos system enabling them to fully decentralize its orderbook and matching engine.

To trade leveraged perpetuals on dYdX, traders first select the asset futures they want to trade (buy the contract for long, sell it for short) and the leverage they’d like to apply. $ETH and $BTC assets allow for up to 20x leverage, while all other assets only allow for up to 10x. Users then deposit the initial margin (all collateral is denominated in $USDC) to open the position.

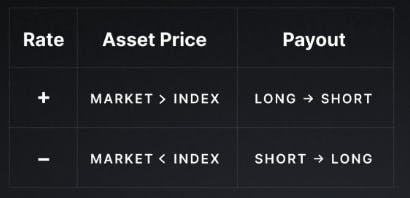

Funding payments are exchanged between long and short traders to encourage the perpetual contract to trade close to the underlying asset. These payments are paid/received based on the funding rate which is adjusted on an 8-hour basis. Generally, if a perpetual trades above the underlying asset’s price, long traders will make payments to short traders. The opposite occurs when the perpetual trades below the underlying: short traders will make payments to long traders. After every hour, the payments are added to/subtracted from a trader’s collateral.

If the value of the perpetual dips below the maintenance margin (collateral needed to keep the position open), a liquidator can liquidate the trader's position in full. What this means is that a liquidator will obtain the trader’s contract. Liquidators also liquidate (obtain) some or all of the trader’s collateral, calculated as the dollar amount the trader purchased the contract for minus the current value of the contract plus a liquidation fee (1% of the current value of the contract) taken from the collateral. The liquidator can then close out the position to make a profit from the liquidation fee.

In the event of extreme market volatility, some accounts may not be liquidated fast enough which would cause the trader’s balance to become negative. To cover the difference, dYdX uses an insurance fund to offset any negative balances. While there is a possibility for decentralization in the future, the dYdX team is directly responsible for depositing and withdrawing into and from the fund.

Tokenomics & Value Accrual

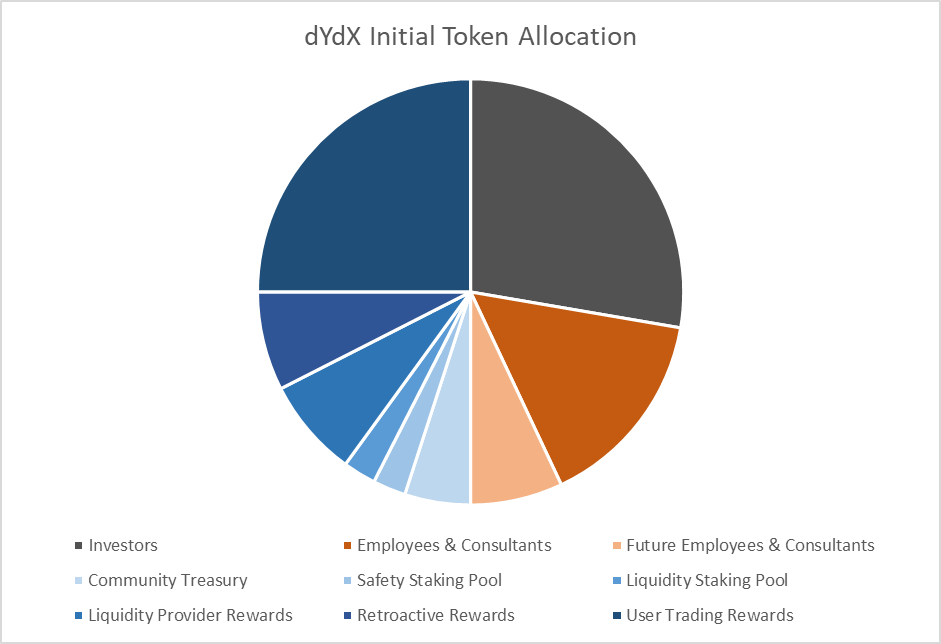

The $DYDX token launched on August 3rd, 2021 with 1 billion tokens minted. These tokens unlock over a five-year period. 27.73% of tokens were allocated to investors (gray section), 22.27% to Founders and the project (orange section), and 50% towards community rewards and airdrops (blue section). After the five-year period, a 2% inflation rate will occur in perpetuity to ensure the community has the resources to continue contributing.

$DYDX can be used to vote on governance proposals and give users trading fee discounts based on the size of their holdings. However, in contrast to some of its competitors, dYdX does not distribute any fee revenue to $DYDX holders. For example one of dYdX’s emerging competitors, GMX, accrues 30% of the platform’s generated fees to $GMX holders.

Revenue, Trading Volume, and Key Metrics Comparison

dYdX charges fees based on the fee schedule shown above on orders that get filled. Maker orders rest on the orderbook for a period of time, while taker orders immediately get filled. This fee revenue is used to pay for transaction expenses and add liquidity.

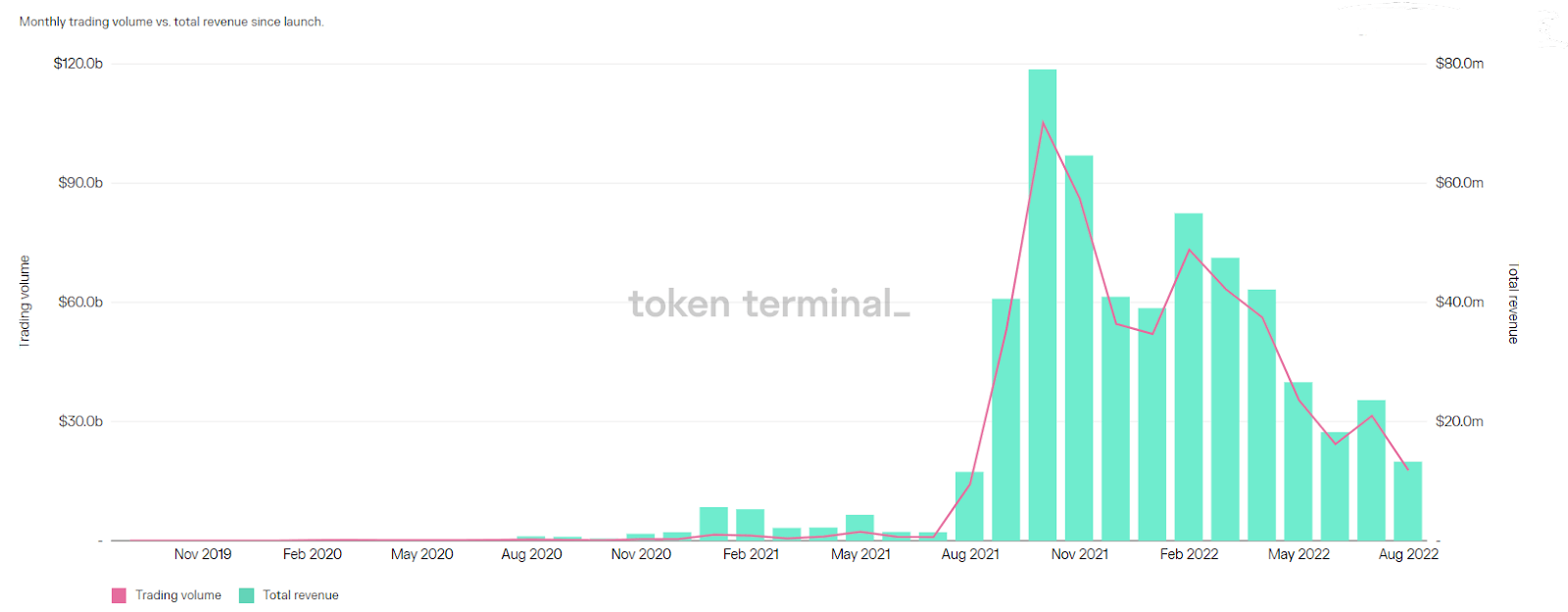

dYdX has annualized total revenue of over $344m and annualized trading volume of over $458b. In addition to this market’s liquidity crunch, with more new competition, dYdX’s total revenue and trading volume have decreased over time.

In comparison, GMX has seen less of a drop off in its monthly revenue. While GMX is smaller (annualized $73m total revenue) and supports fewer assets, its maximum of 30x leverage (compared to dYdX’s 20x) and swap function have allowed it to grow and hold its ground in this market as shown in the graph below.

Governance Process

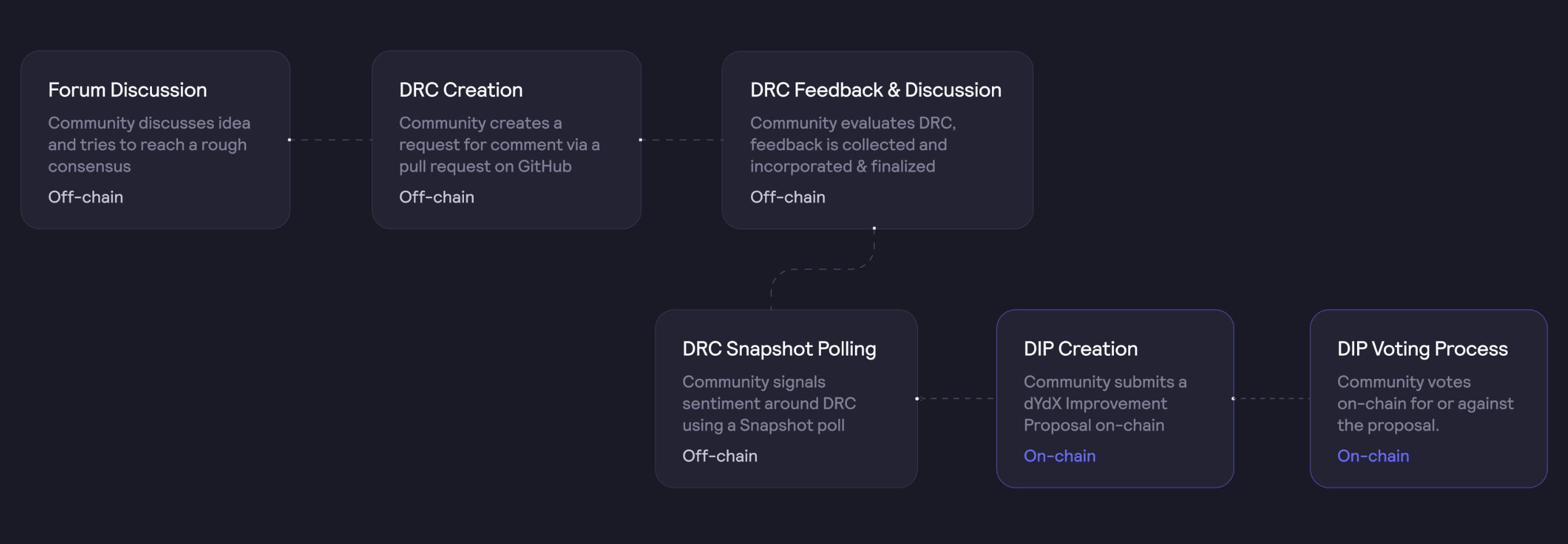

The governance process begins with a discussion on the forms, where anyone can create a thread. After discussions, they can create a DRC (dYdX Request for Comments) using the Github template. There are a few minimum requirements (everything that should be covered in the final dYdX improvement proposal: the DIP), including a short title, description, rationale, and more.

After discussion, feedback, and improvement of the DRC, a community member holding more than 10,000 dYdX (4 wallets as of 9/2/22) can create a snapshot poll. The snapshot poll is the final vote for trading and liquidity provider reward formulas. To pass, a minimum quorum of 1 million $DYDX/stkDYDX is needed and at least 67% of the votes must be in favor of the proposal. dYdX Trading Inc. will then have 28 days to execute a successful snapshot proposal.

For proposals not relating to trading and liquidity provider reward formulas, a community member with a minimum amount of tokens held can create a DIP via a smart contract call. For DIPs relating to the Liquidity Module, Safety Module, funds in the treasuries, minting new tokens, and more (short timelock executor), a minimum of 0.5% of the total supply, or 5,000,000 tokens, (only 21 wallets) are needed to create the DIP, while 2% or 20,000,000 tokens (only 7 wallets), are needed to create a DIP relating to changes in governance consensus (long timelock executor). Short timelock executor proposals need a minimum quorum of 2% and a yes-no gap of 0.5%, while long timelock executor proposals need a minimum quorum of 10% and a yes-no gap of 10%. After passing, a DIP can be queued to be executed.

Latest in Governance

Overall, dYdX’s forums are not incredibly active, but there are some important discussions taking place regarding trading rewards, LP rewards, v4 tokenomics, and the grants program, which is used to fund community NFTs, hackathons, analytics dashboards, memes, swag, third-party tools, translations, and other projects.

Trading and LP Rewards

The most recent Snapshot poll, titled “…More Equitable LP Rewards”, voted to reduce the liquidity provider fee weighting away from BTC and ETH: from 40% (20% for BTC, 20% for ETH), to 20% (10% for BTC, 10% for ETH. This would leave 80% of the rewards for other markets, rather than only 60%. The proposal also allows for other markets to build liquidity and recognizes that the BTC and ETH markets have deep books. The vote ended 19 days ago (as of 9/2/22) and passed with >99%.

Another Snapshot poll titled “Simplifying Trading rewards…”, voted to simplify the trading rewards formula from w = f^(0.8) * d^(0.15) * [Max(10,g)]^(0.05), where w is the individual trader’s score used to determine rewards, f is the total fees paid, d is the trader’s open interest (number of outstanding contracts that haven’t been settled), and g is the trader’s average stkDYDX held, to w = f. The proposal would eliminate the open interest portion of the formula which the proposers allege “adds nothing productive but takes up trading firms margin in order to put on fake large hedged Open Interest positions”. The vote ended around 1 month ago (as of 9/2/22) and passed with >99%.

Cosmos Tokenomics Discussions

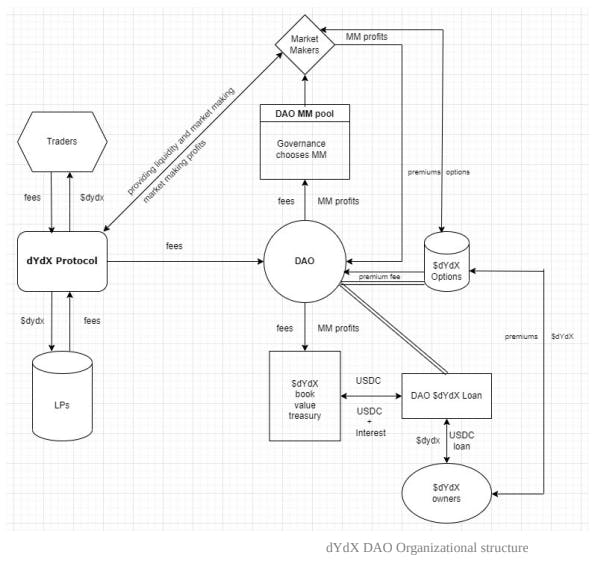

As dYdX begins pivoting to its own chain on Cosmos, many discussions have arisen regarding this change. One such interesting discussion is changes dYdX could make to their DAO structure in order to bring more utility to the $DYDX token. Detailed below, the changes would place 95% of accrued fees in a treasury (the other 5% go to market makers for managing the orderbook). The treasury will always allow dYdX holders to burn their $DYDX tokens for the book value of each $DYDX token (95% of $USDC fee revenue/max $DYDX token supply), allowing the value of the $DYDX token to be in part backed by the $USDC in the treasury (the other part being speculation as to its future revenues). The treasury redemption feature is one part of the proposed model that would help bring more utility to the token by giving holders access to revenues. While this model is not formally endorsed by the dYdX team, it is certainly an interesting hypothetical tokenomics design that shows the potential for dYdX to increase its utility and decentralization.

Risks and Concerns

Centralization Risk

The biggest risk to dYdX is its centralization. Currently, a majority of circulating tokens are held by the team and its investors. It will take until at least 2026 for there to be equal amounts of tokens allocated between the community and the team/investors. dYdX’s governance model also creates a huge barrier to entry by requiring large amounts of tokens to be held to create meaningful proposals to the protocol. Only 21 wallets currently hold enough $DYDX to be able to submit DIPs, most of which are team and investor wallets. In turn, the community has shown little interest in significant protocol changes (because of their lack of influence) and has mostly been involved with rewards formulas (which have a lower holding threshold).

In addition to the lack of community involvement, dYdX’s centralization weakens its ability to add more utility to its governance token, making them a prime target for securities regulatory agencies. The Howey Test, used by the SEC to classify securities, has four main requirements for being a security: 1) It is an investment of money, 2) There is an expectation of profits from the investment, 3) The investment of money is in a common enterprise, and 4) Any profit comes from the efforts of a promoter or third party. If dYdX distributed some of its fee revenue to $DYDX token holders, this could satisfy requirement 4 and the SEC could argue that $DYDX is a security. As discussed above, because the protocol is controlled by the team and not the community, the SEC could allege that profits are coming from a third party. This is opposed to a more decentralized platform where the community has direct control over the management and profit of the investment (the protocol).

Over-Compliance Concerns

After the US Treasury sanctions of Tornado Cash contracts, many dYdX users complained that they had been permanently blocked from accessing dYdX. Some of the blocked users had never even interacted with Tornado Cash. dYdX announced that this was an unintended error and rectified the issue. However, the situation caused brand damage to dYdX and revealed that the team tends to be overly cautious when it comes to compliance since they are not fully decentralized yet.

On August 31st, dYdX announced a new promotional campaign where first-time users received $25 for depositing at least $500. However, in order to qualify for the promotion, dYdX required a “liveness check” that according to dYdX involved scanning “your image using your webcam”. Not surprisingly, this received a large amount of backlash from users in the space as they questioned why dYdX was collecting biometric data for a marketing promotion. The promotional campaign was stopped just 1 day later on September 1st, with the team calling it a success due to overwhelming demand. However, it is too early to tell if this promotional campaign succeeded. While dYdX may have onboarded a large number of new users, it did so at the cost of brand damage and potentially losing defi-native individuals who were upset at the biometric data collecting.

Overall, these recent incidents are concerning developments for the dYdX protocol. It is clear that the dYdX team is becoming over-compliant and willing to make trade-offs for user growth.

Conclusion

With one of the highest revenues and trading volumes among decentralized perpetual protocols, dYdX has positioned itself as the dominant player in the decentralized perpetual space. However, fierce new competition and untimely market conditions have made it especially difficult to maintain its market share. To grow its protocol, dYdX must decrease costs, increase usability, and increase the decentralization of its product. The move to Cosmos could be a promising sign for dYdX as it may help with transaction costs and centralized orderbook issues, but the regulatory risks discussed above may slow the team down if they come to fruition.

Blockchain @ Georgia Tech Socials

If you enjoyed this deep dive stay up to date with Blockchain at Georgia Tech’s upcoming events and posts by following us on Twitter and LinkedIn!

Sources

https://docs.dydx.exchange/#perpetual-contracts

https://docs.dydx.community/dydx-governance/

https://docs.dydx.exchange/#general

https://trade.dydx.exchange/portfolio/overview

https://dydx.exchange/blog/layer-1-wind-down

https://help.dydx.exchange/en/articles/4797401-perpetual-contract-liquidations

https://messari.io/asset/dydx/profile

https://tokenterminal.com/terminal/projects/dydx

https://tokenterminal.com/terminal/projects/gmx

https://twitter.com/adamscochran/status/1565359362612379651?s=21&t=txKCUxQpC6Qb2HeIjX2S9Q